Are you accruing a pension with Zwitserleven through your employer? In that case we will upload a Uniform Benefit Statement (UBS) every year to MijnZwitserleven. It will detail the accrued pension for yourself and the arrangements that will apply in case of your passing or occupational disability. All insurers and pension funds use the same subdivisions for the UBS. It will allow you to easily add up the amounts of pension schemes of the same type.

In MijnZwitserleven you will find your UBS under 'Documents'. You will also find a complete overview of your pension schemes.

Information about your UBS

Your UBS will tell you all about the changes compared with your previous UBS. For example, it will state your standard retirement age. This is the retirement age agreed in your pension scheme. You will also find out how much pension you have already accrued. And the pension you are expected to accrue if you continue to work for the same employer until your standard retirement age.

Your UBS will clearly show whether the partner's pension will be cancelled if you leave your current employer. And you will find information about the consequences of a divorce and where you can get additional information if the Dutch Employee Insurance Agency (UWV) declares you incapacitated for work.

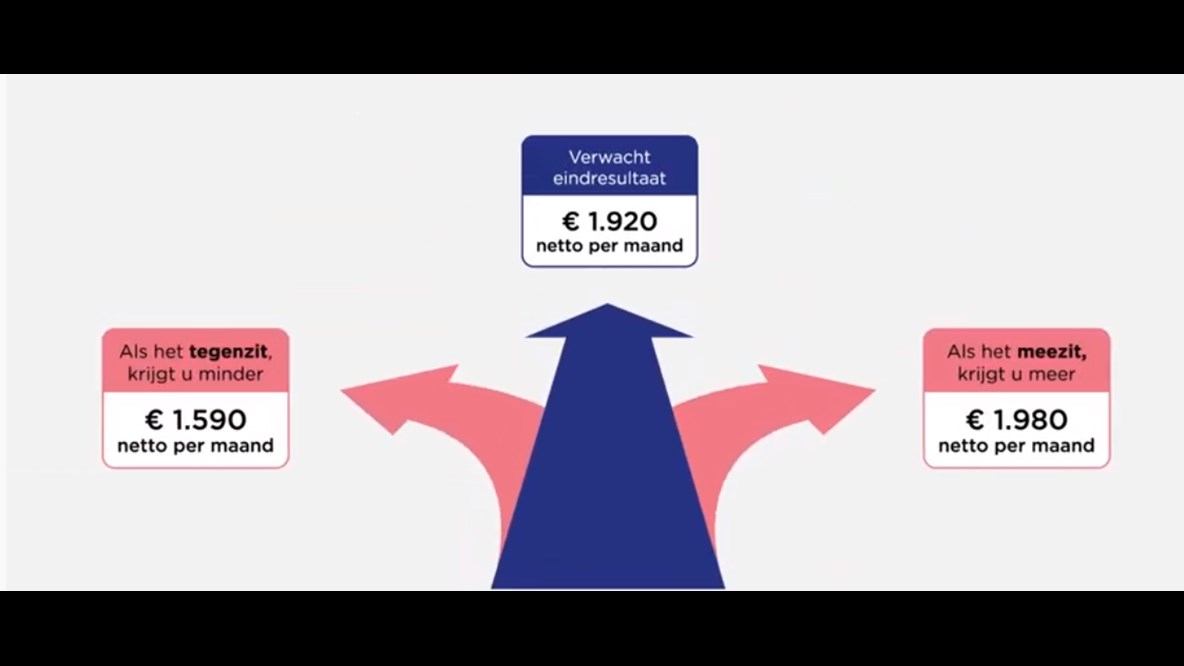

Pension statement also shows best case and worst case

Since September 2019, everyone who accrues a pension has a better understanding of the level of retirement income they can expect. Three different amounts are shown in MijnZwitserleven, each of them calculated according to an expected scenario, a best-case scenario and a worst-case scenario. The scenarios are also shown on the UBS 2020. Watch the video for more information.

Goed om te weten

De drie situaties zijn:

- Als het tegenzit: als het slechter gaat met de economie kun je minder kopen met je pensioen.

- Als het naar verwachting gaat: als de verwachtingen over de economie lijken uit te komen.

- Als het meezit: als het beter gaat met de economie kun je meer kopen met je pensioen.

In deze drie situaties houden we rekening met de volgende punten:

- Alle pensioenuitvoerders gaan uit van dezelfde wettelijke rekenregels. Dat houdt in dat ze onder meer de rentestand, de inflatie en het rendement op de beleggingen toepassen volgens de regels van de URM.

- Bouw je nog pensioen op? Dan houden we tot de afgesproken pensioendatum rekening met:

- Een pensioengrondslag die zich ontwikkelt met de prijsinflatie (dit is het loon dat meetelt voor de pensioenregeling na aftrek van het deel van jouw loon waarover je geen pensioen opbouwt vanwege de AOW).

- Bij middelloon- en eindloonregelingen houden we rekening met de kans op toeslagen op je pensioen. Hoe groot die kans is, hangt af van de afspraken over toeslagen in je pensioenreglement.

- Bij beschikbare premieregelingen met een leeftijdsafhankelijke premie houden we rekening met een mogelijke stijgende beschikbare premie hoe ouder je wordt.